- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 18-03-2019

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | House Price Index (QoQ) | Quarter IV | -1.5% | -2% |

| 00:30 | Australia | RBA Meeting's Minutes | |||

| 07:00 | Switzerland | Trade Balance | February | 1.39 | |

| 09:30 | United Kingdom | Average earnings ex bonuses, 3 m/y | January | 3.4% | 3.4% |

| 09:30 | United Kingdom | Average Earnings, 3m/y | January | 3.4% | 3.2% |

| 09:30 | United Kingdom | ILO Unemployment Rate | January | 4% | 4% |

| 09:30 | United Kingdom | Claimant count | February | 14.2 | 2.7 |

| 09:35 | Eurozone | ECB's Peter Praet Speaks | |||

| 10:00 | Eurozone | Construction Output, y/y | January | 0.7% | 2.1% |

| 10:00 | Eurozone | ZEW Economic Sentiment | March | -16.6 | -18.7 |

| 10:00 | Germany | ZEW Survey - Economic Sentiment | March | -13.4 | -11 |

| 14:00 | U.S. | Factory Orders | January | 0.1% | 0.3% |

| 21:45 | New Zealand | Current Account | Quarter IV | -6.15 | -3.49 |

| 23:50 | Japan | Monetary Policy Meeting Minutes |

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | House Price Index (QoQ) | Quarter IV | -1.5% | -2% |

| 00:30 | Australia | RBA Meeting's Minutes | |||

| 07:00 | Switzerland | Trade Balance | February | 1.39 | |

| 09:30 | United Kingdom | Average earnings ex bonuses, 3 m/y | January | 3.4% | 3.4% |

| 09:30 | United Kingdom | Average Earnings, 3m/y | January | 3.4% | 3.2% |

| 09:30 | United Kingdom | ILO Unemployment Rate | January | 4% | 4% |

| 09:30 | United Kingdom | Claimant count | February | 14.2 | 2.7 |

| 09:35 | Eurozone | ECB's Peter Praet Speaks | |||

| 10:00 | Eurozone | Construction Output, y/y | January | 0.7% | 2.1% |

| 10:00 | Eurozone | ZEW Economic Sentiment | March | -16.6 | -18.7 |

| 10:00 | Germany | ZEW Survey - Economic Sentiment | March | -13.4 | -11 |

| 14:00 | U.S. | Factory Orders | January | 0.1% | 0.3% |

| 21:45 | New Zealand | Current Account | Quarter IV | -6.15 | -3.49 |

| 23:50 | Japan | Monetary Policy Meeting Minutes |

Major US stock indices rose moderately amid a rally in the raw materials sector and expectations of the Fed meeting later this week. .

The two-day Fed meeting on monetary policy starts on Tuesday. According to the FedWatch CME Group tool, markets see zero chance of a rate hike at the March meeting. Nevertheless, investors will look for clues about the estimates of the central bank's economy, as well as the rate of further increase in interest rates.

The focus of market participants was also data on the US housing market. According to a report by the National Association of Home Builders (NAHB), the US Housing Market Condition Index (HMI) remained stable at 62 at March, while economists had forecast growth to 63. According to the report, the HMI component, which reflects sales expectations for the next six months, grew by three points to 71, the index measuring current sales conditions increased by two points to 68, and the component measuring traffic of potential buyers fell by four points to 44.

Most of the components of DOW finished trading in positive territory (21 out of 30). The growth leader was the shares of The Goldman Sachs Group. (GS, + 2.04%). The outsider was The Boeing Co. (UNH; -1.84%).

Almost all sectors of the S & P recorded an increase. The raw materials sector grew the most (+ 1.4%). The health and utility sectors ended the session unchanged.

At the time of closing:

Dow 25,914.10 +65.23 +0.25%

S & P 500 2,832.94 +10.46 +0.37%

Nasdaq 100 7,714.48 +25.95 +0.34%

- We are not in a place to discuss motion and timing for another Brexit vote

- Not in a position to comment on speaker Bercow's statement

- Speaker did not forewarn us of his statement and its content

- If Britain were to participate in European elections, would have to give notice by April 12

- Lawmakers have expressed concerns about being asked to vote on government Brexit deal more than once

- Rules are necessary to ensure sensible use of parliament's time

- Decisions of the House matter, they have weight

The National Association of Homebuilders (NAHB) announced on Monday its housing market index (HMI) held steady at 62 in March, the highest reading since October 2018.

Economists forecast the HMI to increase to 63.

A reading over 50 indicates more builders view conditions as good than poor.

Two out of the three HMI components were higher this month. The index charting sales expectations in the next six months rose 3 points to 71 and the current sales measure increased 2 points to 68. These gains, however, were offset by a 4-point drop in the component measuring traffic of prospective buyers, to 44 in March.

NAHB Chairman Greg Ugalde said: “Builders report the market is stabilizing following the slowdown at the end of 2018 and they anticipate a solid spring home buying season.”

Meanwhile, NAHB Chief Economist Robert Dietz added: “In a healthy sign for the housing market, more builders are saying that lower price points are selling well, and this was reflected in the government’s new home sales report released last week. Increased inventory of affordably priced homes - in markets where government policies support such construction - will enable more entry-level buyers to enter the market.”

- The effects of the idiosyncratic factors currently weighing on economic growth are expected to unwind, albeit at a slower pace than initially foreseen

- Supportive factors continue to be in place that will lift inflation above this year’s muted levels in the more medium term

- Together with the economic expansion, labor cost pressures are expected to trickle through to wage growth and support underlying inflation

- The monetary policy measures announced at the last Governing Council meeting will add to the ECB's already accommodative stance, which will continue to underpin the economic expansion and the convergence of inflation to our medium-term aim

U.S. stock-index flat on Monday, following best weekly performance this year and ahead of the Federal Reserve’s policy meeting later this week.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 21,584.50 | +133.65 | +0.62% |

Hang Seng | 29,409.01 | +396.75 | +1.37% |

Shanghai | 3,096.42 | +74.67 | +2.47% |

S&P/ASX | 6,190.50 | +15.30 | +0.25% |

FTSE | 7,277.78 | +49.50 | +0.68% |

CAC | 5,406.96 | +1.64 | +0.03% |

DAX | 11,647.65 | -38.04 | -0.33% |

Crude | $58.62 | +0.17% | |

Gold | $1,305.90 | +0.23% |

Statistics Canada reported on Monday that foreign investment in Canadian securities rose by CAD 28.4 billion in January 2019, following an upwardly revised CAD 20.49 billion divestment in December (originally -CAD18.96 billion). That was the highest foreign investment since May 2017. According to the report, foreign acquisitions of Canadian debt securities totalled CAD19.4 billion in January and the bulk of the investment was in government debt securities, mainly federal government instruments.

Non-resident investment in federal government bonds reached a record $12.9 billion in January, and mainly targeted secondary market purchases of Canadian dollar-denominated instruments.

Meanwhile, foreign investors cut their holdings of private corporate bonds by CAD 1.3 billion, the second consecutive month of divestment.

Non-resident investors resumed their acquisitions of Canadian money market instruments in January by adding CAD 5.1 billion to their holdings.

Foreign investment in Canadian equities amounted to CAD 9.0 billion in January, the largest investment since February 2017.

Meantime, Canadian investors lowered their holdings of foreign securities by CAD 8.8 billion, led by sales of the U.S. shares.

Guy Verhofstadt, Brexit coordinator for the European Parliament told the Standard that the UK could be refused a Brexit extension if Prime minister May fails to get agreement in the Commons.

According to him, the UK needs a cross-party agreement and to put “country before party” prior to seeking an extension of Article 50.

“Why should the EU27 even consider a Brexit extension this week, if the UK parliament vote on the deal is cancelled?” he said. “Where are the cross-party talks?

He also added that "it is time for country to come before party. A minority of Right-wing populists cannot be allowed to drive European citizens and businesses off a cliff.”

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALTRIA GROUP INC. | MO | 56.71 | -0.04(-0.07%) | 1176849 |

Amazon.com Inc., NASDAQ | AMZN | 1,713.50 | 1.14(0.07%) | 30007 |

Apple Inc. | AAPL | 186.18 | 0.06(0.03%) | 143939 |

AT&T Inc | T | 30.73 | 0.06(0.20%) | 36262 |

Boeing Co | BA | 370 | -8.99(-2.37%) | 365506 |

Caterpillar Inc | CAT | 132 | -0.67(-0.51%) | 102285 |

Chevron Corp | CVX | 125.5 | 0.19(0.15%) | 5318 |

Cisco Systems Inc | CSCO | 53.3 | 0.10(0.19%) | 26334 |

Citigroup Inc., NYSE | C | 65.31 | 0.12(0.18%) | 10616 |

Facebook, Inc. | FB | 164.65 | -1.33(-0.80%) | 140937 |

FedEx Corporation, NYSE | FDX | 178.93 | 0.95(0.53%) | 2385 |

Ford Motor Co. | F | 8.44 | 0.01(0.12%) | 26118 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 12.48 | 0.13(1.05%) | 18094 |

General Electric Co | GE | 9.99 | 0.03(0.30%) | 145695 |

General Motors Company, NYSE | GM | 38.08 | 0.01(0.03%) | 3126 |

Google Inc. | GOOG | 1,185.04 | 0.58(0.05%) | 3427 |

Hewlett-Packard Co. | HPQ | 19.88 | -0.06(-0.30%) | 4918 |

Home Depot Inc | HD | 182.51 | 0.28(0.15%) | 3680 |

Intel Corp | INTC | 54.45 | 0.12(0.22%) | 21590 |

International Business Machines Co... | IBM | 139.78 | 0.35(0.25%) | 2636 |

International Paper Company | IP | 45.99 | 0.48(1.05%) | 4464 |

Johnson & Johnson | JNJ | 137.81 | 0.21(0.15%) | 7318 |

JPMorgan Chase and Co | JPM | 106.66 | 0.11(0.10%) | 805386 |

McDonald's Corp | MCD | 185.76 | 0.43(0.23%) | 4038 |

Microsoft Corp | MSFT | 116.15 | 0.24(0.21%) | 73842 |

Nike | NKE | 87.4 | 0.60(0.69%) | 8949 |

Pfizer Inc | PFE | 41.68 | -0.10(-0.24%) | 17134 |

Procter & Gamble Co | PG | 102.69 | 0.25(0.24%) | 6441 |

Starbucks Corporation, NASDAQ | SBUX | 70.99 | 0.32(0.45%) | 4585 |

Tesla Motors, Inc., NASDAQ | TSLA | 275.77 | 0.34(0.12%) | 67319 |

The Coca-Cola Co | KO | 45.44 | 0.14(0.31%) | 13818 |

Twitter, Inc., NYSE | TWTR | 31.21 | -0.01(-0.03%) | 25724 |

UnitedHealth Group Inc | UNH | 251.41 | 0.01(0.00%) | 2905 |

Verizon Communications Inc | VZ | 58.45 | 0.06(0.10%) | 10478 |

Visa | V | 156.2 | 0.74(0.48%) | 13207 |

Wal-Mart Stores Inc | WMT | 98.41 | -0.01(-0.01%) | 4992 |

Walt Disney Co | DIS | 112.79 | -2.17(-1.89%) | 232303 |

Yandex N.V., NASDAQ | YNDX | 36.9 | 0.92(2.56%) | 14220 |

NIKE (NKE) target raised to $95 from $92 at Telsey Advisory Group

- Government prefers short, technical Brexit extension

- If vote fails this week, will seek a longer extension

- UK will then have to take part in the European parliament elections

- Brexit date can be changed with secondary legislation

- Government is still preparing for no-deal Brexit

BBC's Europe editor, Katya Adler, tweeted: "Whisper it quietly but suggestions in some EU quarters of possible EU leaders emergency #Brexit summit on 28 March .. Depending on how/when/how many ‘meaningful votes’ there are in Parliament between now and then. Though little evidence of appetite for said extra summit."

The Bundesbank said in its monthly report on Monday that German economic growth remained subdued in the first quarter.

According to the bank, the major draggers behind this subdued performance were weak industrial production, falling export demand for cars and deteriorating manufacturing sentiment.

Struggling with unexpected weakness in among its car manufacturers, Germany barely escaped a recession last quarter, the Bundesbank said in the report.

The regulator also noted that fresh indicators suggest any recovery will be slow, at best, a drag on growth across the entire Eurozone.

- OPEC+ needs a few months to drain excess inventory

- No OPEC+ meeting in April, the next one to be in June

- The next meeting of the Joint Ministerial Monitoring Committee (JMMC) is likely in the first half of May; date to be announced in the next two weeks

- Inventory glut needs to be drained before cuts are ended

- We will swing our oil production if necessary

- Expect inventory drop between now and May

Danske Bank analysts are expecting that the US Fed will likely keep the target range unchanged at 2.25-2.50% and make no major changes to the statement in its forthcoming meeting this Wednesday.

We expect Fed to lower its 'dot' signal further to just one rate hike in 2019 (down from two) .

We expect them to be revised lower also for 2020 and 2021 and we will not be surprised if the Fed signals "one and done".

We expect the longer-run dot is to be unchanged at 2.75%.

Our current base case is two Fed hikes (in June and December) based on our overall positive economic outlook.

However, if the Fed confirms it has changed its reaction function by looking more at inflation expectations and less on the unemployment rate, a June hike seems less likely

We believe the Fed will announce it will end shrinking its balance sheet in Q4.

SEB Bank analysts points out that the US Fed will present its first updated forecasts after its U-turn in Jan on Wednesday and will be a key event for markets this week.

“We expect relatively small changes to its economic forecasts but “dot plots” to shift from two hikes in 2019 to unchanged rates. Given the dovish market pricing (5bps rate cut by end-19), this should have limited impact on markets and we see risks to US rates being biased somewhat on the upside. In light of our expectations of an improving outlook we stick to our forecast that the Fed will deliver a final rate hike in June.”

According to the report from Eurostat, the first estimate for euro area (EA19) exports of goods to the rest of the world in January 2019 was €183.4 billion, an increase of 2.5% compared with January 2018 (€179.0 bn). Imports from the rest of the world stood at €181.8 bn, a rise of 3.4% compared with January 2018 (€175.9 bn). As a result, the euro area recorded a €1.5 bn surplus in trade in goods with the rest of the world in January 2019, compared with +€3.1 bn in January 2018. Intra-euro area trade rose to €164.6 bn in January 2019, up by 2.4% compared with January 2018.

In 2018, euro area exports of goods to the rest of the world rose to €2 277.6 bn (an increase of 3.7% compared with 2017), and imports rose to €2 084.2 bn (an increase of 6.6% with respect to the previous year). As a result the euro area recorded a surplus of €193.4 bn in 2018, compared with +€240.8 bn in 2017. Intra-euro area trade rose to €1 943.5 bn in 2018, up by 5.3% compared with 2017.

Britain’s government will only hold another meaningful vote on Prime Minister Theresa May’s Brexit deal on Tuesday if it is certain that the divided House of Commons would back it at a third attempt, the foreign minister said.

Jeremy Hunt told journalists on Monday when asked if the vote would take place the following day: “We hope it will. But we need to be comfortable that we’ll have the numbers.”

“The risk of no-deal, at least as far as the UK parliament is concerned, has receded somewhat but the risk of Brexit paralysis has not,” said Hunt, added there were “cautious signs of encouragement” that May’s deal could go through.

The European Union will seek Beijing's agreement for deadlines to open up China's economy at an April 9 summit in Brussels, trying to coax it into making good on promises to deepen trade ties, according to a draft leaders' statement.

China and the EU will "agree by summer 2019 on a set of priority market access barriers and requirements facing their operators," according to a six-page joint communique drafted by the EU, which still requires Chinese approval.

UK GDP rebounded nicely to start 2019, after a sharp slowing in December as manufacturing, construction, and services output all increased in January to retrace the previous month’s declines, explains the analysis team at Royal Bank of Canada.

“The monthly data can be volatile, but this latest reading will help allay fears that the UK economy is grinding to a halt amid Brexit uncertainty. Still, survey data point to Brexit continuing to weigh on business sentiment. On balance, our forecast assumes we’ll see another quarter of subtrend 0.2% growth to start this year.”

grey rhino risks in key areas are rising

risks in local government hidden debt, bond defaults and property market could trigger financial risks

should prevent household leverage ratios too fast

stability of yuan exchange rate, forex reserves faces pressure

will step up monitoring of stock, bond, forex markets

According to a new Bloomberg survey of economists, Fed will bring the current cycle of interest-rate increases to an end after one more hike later this year,

The median of responses in the March 13-15 poll predicted one hike in September, compared with two 2019 increases forecast in the December survey. They also said that would likely mark the peak of this hiking cycle, with the upper end of the target range for the benchmark rate touching 2.75%. Just three months ago they saw that peak at 3.25%.

None of the 32 respondents anticipated a rate move when the Fed gathers March 19-20. Fed officials have repeatedly signaled they are content to leave rates unchanged this month and perhaps well into 2019.

According to Karen Jones, analyst at Commerzbank, USD/JPY pair is neutralising near term and it is possible that will have to allow for a deeper retracement to the 55 day MA and the 2 month uptrend at 110.08/110.13, which should hold for an upside bias to be preserved.

“We suspect that it is trying to reassert its up move sooner. Immediate resistance is 112.23, the 6th December low, the 112.43 55 quarter moving average and recent high at 113.71. We have a 5 month resistance line also at 113.08. Long term trend (1-3 months): break of the 200 day MA opens path to the 113.71 recent high and the top of the range at 114.55/73.”

Top U.S. business leaders are “bracing for a recession,” and many are already starting to slash costs to prepare their companies for a downturn ahead.

So says the research firm Gartner, after a study of all the recent fourth-quarter corporate results announcements, and the transcripts of business leaders’ earnings calls with Wall Street analysts.

“Many of the world’s largest companies are starting to behave as if they are in a recession. A significant number of leading firms are taking a recessionary stance and making preparations to capitalize on a downturn rather than be a casualty of one,” said Tim Raiswell, vice president of Gartner’s finance practice.

Raiswell said that U.S. executives were still offering a “broadly positive” outlook for the economy. But more and more are talking about a possible “downturn” or “recession,” and have announced efficiency measures to cut costs.

Bank executives have sounded the alarm about the rise in risky consumer lending by nonbank providers, Gartner found.

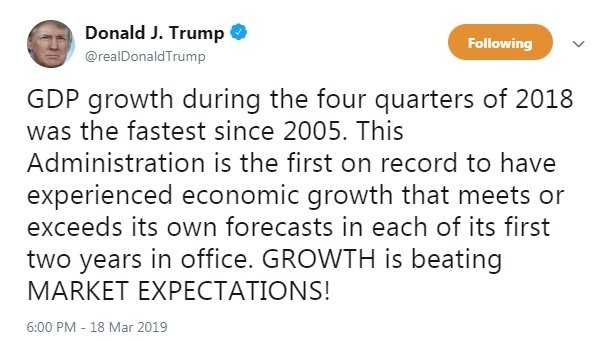

And corporate leaders across the board are worried about the turmoil in Washington and a sharp slowdown in the Chinese economy. Donald Trump’s intermittent saber rattling against China over trade, along with the recent government shutdown and overseas problems like Brexit, are also factors.

Danske Bank analysts suggest that later in the week, central banks will dominate the agenda with the BOE, Fed and Norges Bank concluding their policy meetings.

“The week starts out on a fairly quiet note with regards to economic releases. Instead markets will be looking for new signals from Brussels with regard to the extension of the triggering of Article 50 in relation to Brexit. On Wednesday, the Fed is on hold while lowering the 'dot' signal for 2019 to one hike (from two), and hence we think the most interesting meeting will be the Norges Bank meeting on Thursday, where we expect a rise in its policy rate by 25bp to 1.00% and to signal one further rate hike this year.”

Karen Jones, analyst at Commerzbank, points out that the GBP/USD pair continues to hold and bounce from the short term uptrend at 1.3002, after the market last week challenged the 1.3363 July 2018 high, reaching 1.3382 before failing.

“The new high has been accompanied by a divergence of the daily RSI and we would allow for some near term consolidation ahead of further upside attempts. Overall target remains the 1.3574 200 week MA. Below the 1.3002 short term uptrend lies the double Fibo retracement at 1.2900/1.2895. This guards the recent low at 1.2772. Below 1.2772 we would allow for losses to the 1.2669/62 15th January low and August low and possibly the 1.2609/78.6% retracement.”

The British Chambers of Commerce (BCC) has today slightly downgraded its growth expectations for the UK economy, forecasting growth of just 1.2% in 2019 (down from 1.3%), which if realised would be the weakest growth in a decade. The BCC has also downgraded its growth forecast for 2020 to 1.3% (down from 1.5%) and published its first forecast for 2021 of 1.4% growth.

A weaker outlook for business investment and trade amid continued Brexit uncertainty and slower expected global economic growth were the main drivers behind the leading business group’s downgrades to its forecast for GDP growth in 2019 and 2020.

Key points in the forecast:

Business investment is expected to contract by -1.0% in 2019, before returning to growth of 0.6% in 2020 and 1.1% in 2021

Growth in household consumption for 2019 is expected to slow to 1.3%, before rising slightly to 1.4% in 2020 and 1.5% in 2021

Average earnings growth is forecast to outstrip inflation over the period, with growth of 2.9%, 3.0%, and 3.1%, compared with inflation of 2.1%, 2.0%, and 1.9%

UK official interest rates are expected to remain on hold throughout 2019, before increasing to 1.0% in Q2 2020. This is three quarters later than predicted in our Q4 forecast

EUR/USD

Resistance levels (open interest**, contracts)

$1.1460 (1721)

$1.1440 (1336)

$1.1418 (366)

Price at time of writing this review: $1.1336

Support levels (open interest**, contracts):

$1.1281 (3834)

$1.1240 (3068)

$1.1194 (2831)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date April, 5 is 71257 contracts (according to data from March, 15) with the maximum number of contracts with strike price $1,1550 (4520);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3433 (6366)

$1.3407 (420)

$1.3381 (793)

Price at time of writing this review: $1.3284

Support levels (open interest**, contracts):

$1.3182 (261)

$1.3155 (388)

$1.3126 (1093)

Comments:

- Overall open interest on the CALL options with the expiration date April, 5 is 23811 contracts, with the maximum number of contracts with strike price $1,3400 (4419);

- Overall open interest on the PUT options with the expiration date April, 5 is 25660 contracts, with the maximum number of contracts with strike price $1,2500 (3628);

- The ratio of PUT/CALL was 1.08 versus 1.08 from the previous trading day according to data from March, 15

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 66.92 | -0.21 |

| WTI | 58.65 | -0.17 |

| Silver | 15.26 | 0.59 |

| Gold | 1301.964 | 0.45 |

| Palladium | 1550.24 | 0.01 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | 163.83 | 21450.85 | 0.77 |

| Hang Seng | 160.87 | 29012.26 | 0.56 |

| KOSPI | 20.43 | 2176.11 | 0.95 |

| ASX 200 | -4.4 | 6175.2 | -0.07 |

| FTSE 100 | 42.85 | 7228.28 | 0.6 |

| DAX | 98.22 | 11685.69 | 0.85 |

| CAC 40 | 55.54 | 5405.32 | 1.04 |

| Dow Jones | 138.93 | 25848.87 | 0.54 |

| S&P 500 | 14 | 2822.48 | 0.5 |

| NASDAQ Composite | 57.62 | 7688.53 | 0.76 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.7081 | 0.24 |

| EURJPY | 126.221 | 0.01 |

| EURUSD | 1.13235 | 0.18 |

| GBPJPY | 148.148 | 0.09 |

| GBPUSD | 1.32885 | 0.23 |

| NZDUSD | 0.68418 | 0.13 |

| USDCAD | 1.33335 | 0.02 |

| USDCHF | 1.00198 | -0.17 |

| USDJPY | 111.434 | -0.19 |

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers