- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 06-02-2018

(raw materials / closing price /% change)

Oil 63.92 -0.36%

Gold 1,326.90 -0.72%

(index / closing price / change items /% change)

Nikkei -1071.84 21610.24 -4.73%

TOPIX -80.33 1743.41 -4.40%

Hang Seng -1649.80 30595.42 -5.12%

CSI 300 -125.26 4148.89 -2.93%

Euro Stoxx 50 -83.85 3394.92 -2.41%

FTSE 100 -193.58 7141.40 -2.64%

DAX -294.83 12392.66 -2.32%

CAC 40 -124.02 5161.81 -2.35%

DJIA +567.02 24912.77 +2.33%

S&P 500 +46.20 2695.14 +1.74%

NASDAQ +148.36 7115.88 +2.13%

S&P/TSX +29.12 15363.93 +0.19%

(pare/closed(GMT +2)/change, %)

EUR/USD $1,2376 +0,08%

GBP/USD $1,3950 -0,05%

USD/CHF Chf0,93605 +0,47%

USD/JPY Y109,55 +0,38%

EUR/JPY Y135,59 +0,46%

GBP/JPY Y152,831 +0,32%

AUD/USD $0,7905 +0,36%

NZD/USD $0,7340 +1,04%

USD/CAD C$1,24933 -0,37%

00:00 Japan Labor Cash Earnings, YoY December 0.9% 0.7%

05:00 Japan Leading Economic Index (Preliminary) December 108.3 108.1

05:00 Japan Coincident Index (Preliminary) December 117.9 118.2

07:00 Germany Industrial Production s.a. (MoM) December 3.4% -0.5%

07:45 France Trade Balance, bln December -5.7 -4.9

08:00 Switzerland Foreign Currency Reserves January 744

08:30 United Kingdom Halifax house price index 3m Y/Y January 2.7% 2.4%

08:30 United Kingdom Halifax house price index January -0.6% 0.2%

09:00 Eurozone ECB's Lautenschläger Speech

13:30 Canada Building Permits (MoM) December -7.7% 2%

13:30 U.S. FOMC Member Dudley Speak

15:30 U.S. Crude Oil Inventories February 6.776 2.86

16:15 U.S. FOMC Member Charles Evans Speaks

20:00 New Zealand RBNZ Interest Rate Decision 1.75% 1.75%

20:00 New Zealand RBNZ Rate Statement

20:00 U.S. Consumer Credit December 27.95 20

21:00 New Zealand RBNZ Press Conference

22:20 U.S. FOMC Member Williams Speaks

23:50 Japan Current Account, bln December 1.347 1017.5

Major US stock indices rose strongly on Tuesday, partially recovering from the biggest one-day drop in S & P and Dow in more than 6 years. Support for the indices was exacerbated by increased risk aversion, as well as the fading of fears over inflation and higher yields on government bonds

Negligible impact on the course of trading also provided data on the United States. As shown today, the survey of vacancies and labor turnover (JOLTS), published by the Bureau of Labor Statistics in the US, in December the number of vacancies fell to 5.811 million. Meanwhile, the indicator for November was revised upwards to 5.978 million from 5.879 million. Analysts had expected, that the number of vacancies will decrease to 5.9 million. The vacancy rate was 3.8%, decreasing by 0.1% compared to November. The number of vacancies has changed little in both the private sector and the government segment.

Quotes of oil fell by about 1% on Tuesday, covered by the latest wave of sales, which dealt a blow to the stock markets, bonds, crypto-currencies, and commodities. Even though Wall Street stocks recorded their biggest one-day drop since late 2011 on Monday and volatility indicators jumped to multi-year highs, reflecting increased nervousness among investors, oil did not suffer to the same extent.

Most components of the DOW index finished in positive territory (26 out of 30). The leader of growth was the shares of DowDuPont Inc. (DWDP, + 5.97%). Outsider were shares of Exxon Mobil Corporation (XOM, -1.76%).

Almost all sectors of the S & P index recorded an increase. The consumer goods sector grew most (+ 2.0%). The decrease was shown only by the utilities sector (-0.8%).

At closing:

DJIA + 2.33% 24,912.77 +567.02

Nasdaq + 2.13% 7,115.88 +148.36

S & P + 1.74% 2,695.14 +46.20

The number of job openings was little changed at 5.8 million on the last business day of December, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.5 million and 5.2 million, respectively. Within separations, the quits rate and the layoffs

and discharges rate were little changed at 2.2 percent and 1.1 percent, respectively. This release includes estimates of the number and rate of job openings, hires, and separations for the nonfarm sector by industry and by four geographic regions.

U.S. stock-index futures were mixed on Tuesday after big losses in the previous two trading sessions.

Global Stocks:

Nikkei 21,610.24 -1,071.84 -4.73%

Hang Seng 30,595.42 -1,649.80 -5.12%

Shanghai 3,369.71 -117.79 -3.38%

S&P/ASX 5,833.30 -192.90 -3.20%

FTSE 7,183.20 -151.78 -2.07%

CAC 5,137.49 -148.34 -2.81%

DAX 12,379.25 -308.24 -2.43%

Crude $63.47 (-1.06%)

Gold $1,336.80 (+0.02%)

Imports rose 1.5% and exports were up 0.6%, both led by energy products.

Total imports were up 1.5% to a record $49.7 billion in December, with increases in 9 of 11 sections. Volumes rose 1.0% and prices increased 0.5%. Higher imports of energy products and industrial machinery, equipment and parts were partially offset by lower imports of aircraft and other transportation equipment and parts.

Total exports rose for the third consecutive month, up 0.6% to $46.5 billion in December despite decreases in 6 of 11 sections. Prices were up 0.5% while volumes were essentially unchanged. Higher exports of energy products, and metal and non-metallic mineral products were partially offset by lower exports of consumer goods. Exports excluding energy products decreased 0.6%.

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $53.1 billion in December, up $2.7 billion from $50.4 billion in November, revised. December exports were $203.4 billion, $3.5 billion more

than November exports. December imports were $256.5 billion, $6.2 billion more than November imports.

The December increase in the goods and services deficit reflected an increase in the goods deficit of $2.6 billion to $73.3 billion and a decrease in the services surplus of $0.1 billion to $20.2 billion.

For 2017, the goods and services deficit increased $61.2 billion, or 12.1 percent, from 2016. Exports increased $121.2 billion or 5.5 percent. Imports increased $182.5 billion or 6.7 percent.

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 225.05 | -6.39(-2.76%) | 16802 |

| ALCOA INC. | AA | 47.89 | -0.57(-1.18%) | 1512 |

| ALTRIA GROUP INC. | MO | 65.05 | -0.99(-1.50%) | 9377 |

| Amazon.com Inc., NASDAQ | AMZN | 1,361.50 | -28.50(-2.05%) | 158802 |

| American Express Co | AXP | 87.54 | -4.47(-4.86%) | 11259 |

| AMERICAN INTERNATIONAL GROUP | AIG | 59.21 | -1.42(-2.34%) | 13134 |

| Apple Inc. | AAPL | 154.93 | -1.56(-1.00%) | 555093 |

| AT&T Inc | T | 36.06 | -0.57(-1.56%) | 120697 |

| Barrick Gold Corporation, NYSE | ABX | 13.52 | -0.11(-0.81%) | 8040 |

| Boeing Co | BA | 318.49 | -10.39(-3.16%) | 91669 |

| Caterpillar Inc | CAT | 145.1 | -5.98(-3.96%) | 51837 |

| Chevron Corp | CVX | 110.8 | -1.82(-1.62%) | 22354 |

| Cisco Systems Inc | CSCO | 38.23 | -0.55(-1.42%) | 106380 |

| Citigroup Inc., NYSE | C | 70.97 | -2.30(-3.14%) | 96719 |

| Exxon Mobil Corp | XOM | 78.53 | -1.19(-1.49%) | 126179 |

| Facebook, Inc. | FB | 178.5 | -2.76(-1.52%) | 607679 |

| FedEx Corporation, NYSE | FDX | 242.6 | -5.90(-2.37%) | 1417 |

| Ford Motor Co. | F | 10.12 | -0.12(-1.17%) | 213411 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 17.3 | -0.35(-1.98%) | 32292 |

| General Electric Co | GE | 14.77 | -0.14(-0.94%) | 520638 |

| General Motors Company, NYSE | GM | 39.39 | -0.15(-0.38%) | 297145 |

| Goldman Sachs | GS | 243.1 | -6.01(-2.41%) | 44199 |

| Google Inc. | GOOG | 1,030.95 | -24.85(-2.35%) | 28177 |

| Hewlett-Packard Co. | HPQ | 20.71 | -0.58(-2.72%) | 10898 |

| Home Depot Inc | HD | 177.27 | -5.84(-3.19%) | 27070 |

| HONEYWELL INTERNATIONAL INC. | HON | 146.67 | -3.50(-2.33%) | 1557 |

| Intel Corp | INTC | 43.8 | -0.42(-0.95%) | 89037 |

| International Business Machines Co... | IBM | 150.8 | -1.73(-1.13%) | 28888 |

| Johnson & Johnson | JNJ | 128.52 | -1.87(-1.43%) | 30124 |

| JPMorgan Chase and Co | JPM | 105.87 | -2.93(-2.69%) | 59688 |

| McDonald's Corp | MCD | 157.3 | -6.55(-4.00%) | 26969 |

| Merck & Co Inc | MRK | 55.06 | -1.34(-2.38%) | 19467 |

| Microsoft Corp | MSFT | 87.23 | -0.77(-0.88%) | 306903 |

| Nike | NKE | 62.55 | -1.84(-2.86%) | 53698 |

| Pfizer Inc | PFE | 34.16 | -0.51(-1.47%) | 46202 |

| Procter & Gamble Co | PG | 80 | -1.06(-1.31%) | 39319 |

| Starbucks Corporation, NASDAQ | SBUX | 53.56 | -1.13(-2.07%) | 23897 |

| Tesla Motors, Inc., NASDAQ | TSLA | 325.55 | -7.58(-2.28%) | 77262 |

| The Coca-Cola Co | KO | 44.07 | -0.82(-1.83%) | 26523 |

| Travelers Companies Inc | TRV | 134.91 | -6.61(-4.67%) | 9119 |

| Twitter, Inc., NYSE | TWTR | 24.5 | -0.63(-2.51%) | 168996 |

| United Technologies Corp | UTX | 124.15 | -3.09(-2.43%) | 20034 |

| UnitedHealth Group Inc | UNH | 212 | -8.02(-3.65%) | 16166 |

| Verizon Communications Inc | VZ | 49.6 | -0.90(-1.78%) | 19987 |

| Visa | V | 114.46 | -1.81(-1.56%) | 277412 |

| Wal-Mart Stores Inc | WMT | 98.35 | -1.74(-1.74%) | 34439 |

| Walt Disney Co | DIS | 102.24 | -2.46(-2.35%) | 85276 |

Freeport-McMoRan (FCX) target raised to $18 at Stifel

Exxon Mobil (XOM) downgraded to Underweight from Equal Weight at Barclays

Chevron (CVX) upgraded to Overweight from Equal Weight at Barclays

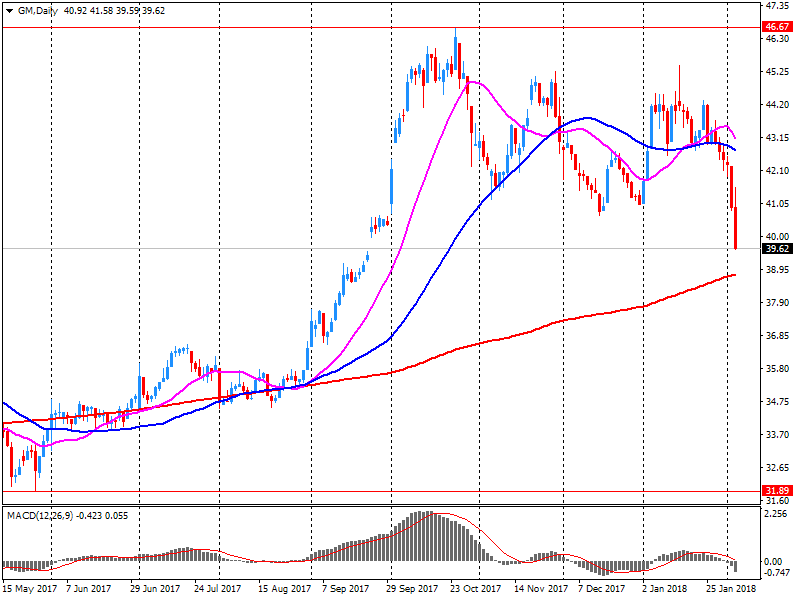

General Motors (GM) reported Q4 FY 2017 earnings of $1.65 per share (versus $1.28 in Q4 FY 2016), beating analysts' consensus estimate of $1.43.

The company's quarterly revenues amounted to $34.481 bln (-7.7% y/y), generally in-line with analysts' consensus estimate of $34.280 bln.

GM rose to $40.20 (+1.44%) in pre-market trading.

-

Says hard to say if EU, rather than Britain, would be worse off with no post-brexit financial services agreement

-

FPC is "very much" alive to potential risks from UK consumer credit growth

-

Commercial real estate in prime central London is very fully valued

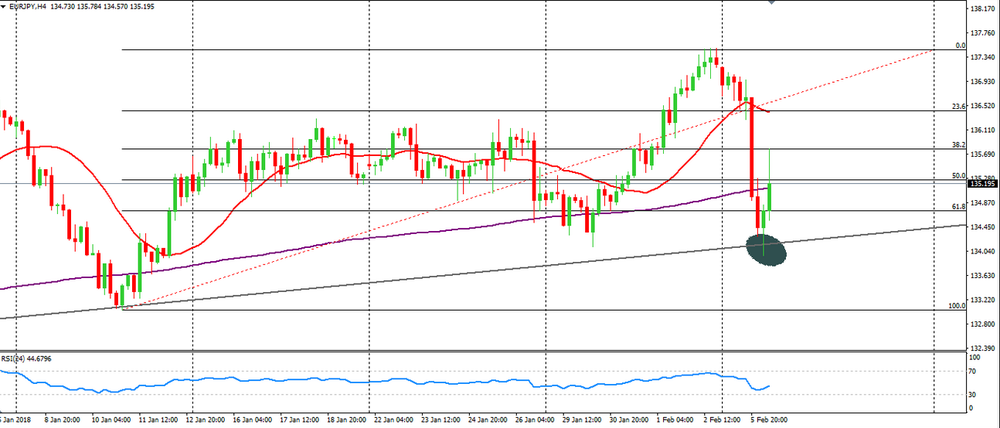

EUR/JPY has suffered a huge depreciation earlier in this week, largely due to recent stock-market corrections.

However, if we look at the 4-hour time frame chart, we can see that the price gave clear signs of a rejection of Fibonacci levels and the upside trend line that has been forming below the price.

Therefore, if the price continues to reject further down movements then we can expect a new appreciation on EUR/JPY.

The headline IHS Markit Eurozone Retail PMI - which tracks the month-on-month changes in retail sales in the bloc‟s biggest three economies combined - fell to 50.8 in January, from 53.0 in December. Sales were down on an annual basis after having been broadly unchanged in December.

Alex Gill, economist at IHS Markit which compiles the Eurozone Retail PMI, said: "The latest data paint a mixed picture as to the overall health of the eurozone retail sector. On the one hand, like-for-like sales and employment continued to rise, albeit at weaker rates than seen in December. On the other, sales remained down on an annual basis, gross margins were squeezed further while weaker than expected sales contributed to a build-up of inventories.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2551 (2563)

$1.2526 (1505)

$1.2486 (4025)

Price at time of writing this review: $1.2395

Support levels (open interest**, contracts):

$1.2338 (3383)

$1.2294 (4413)

$1.2247 (4926)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 9 is 143659 contracts (according to data from February, 5) with the maximum number of contracts with strike price $1,1850 (7036);

GBP/USD

Resistance levels (open interest**, contracts)

$1.4211 (982)

$1.4181 (1698)

$1.4154 (3462)

Price at time of writing this review: $1.3944

Support levels (open interest**, contracts):

$1.3887 (757)

$1.3841 (1202)

$1.3794 (1013)

Comments:

- Overall open interest on the CALL options with the expiration date February, 9 is 40952 contracts, with the maximum number of contracts with strike price $1,3600 (3462);

- Overall open interest on the PUT options with the expiration date February, 9 is 37589 contracts, with the maximum number of contracts with strike price $1,3400 (3038);

- The ratio of PUT/CALL was 0.92 versus 0.92 from the previous trading day according to data from February, 5

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Inappropriate to shift monetary policy prematurely just to create future policy tools

-

BoJ will take appropriate steps to boost cyber-resilience, support private-sector efforts to protect market infrastructure

-

Cyber attacks against market infrastructure could pose huge shock to financial system that could spread to global markets

-

Providers of cryptocurrency-related services must proactively take steps to boost security, explain risks involved to investors

-

Cryptocurrencies currently used mostly for investment, speculative trading with usage for settlement rare

Balance on goods and services:

-

In trend terms, the balance on goods and services was a deficit of $476m in december 2017, an increase of $313m on the deficit in november 2017.

-

In seasonally adjusted terms, the balance on goods and services was a deficit of $1,358m in december 2017, a turnaround of $1,394m on the surplus in november 2017.

Credits (exports of goods and services):

In seasonally adjusted terms, goods and services credits rose $510m (2%) to $32,465m. Non-rural goods rose $719m (4%). Rural goods fell $144m (4%), non-monetary gold fell $9m (1%) and net exports of goods under merchanting fell $1m (2%). Services credits fell $54m (1%).

Australian retail turnover fell 0.5 per cent in December 2017, seasonally adjusted, according to the latest Australian Bureau of Statistics (ABS) Retail Trade figures.

This follows a 1.3 per cent rise in November 2017.

"There were falls for household goods retailing (-2.6 per cent) and other retailing (-1.8 per cent) following strong rises in the November month," said Ben James, Director of Quarterly Economy Wide Surveys. "Department stores (-0.6 per cent), cafes, restaurants and takeaways (-0.1 per cent), and clothing, footwear and personal accessory retailing (-0.1 per cent) also fell. Food retailing rose (0.7 per cent) in December 2017."

In seasonally adjusted terms, there were falls in Victoria (-0.8 per cent), New South Wales (-0.4 per cent), Western Australia (-0.8 per cent), Tasmania (-1.6 per cent), the Australian Capital Territory (-1.5 per cent), South Australia (-0.3 per cent), and the Northern Territory (-0.7 per cent). Queensland was relatively unchanged (0.0 per cent) in seasonally adjusted terms.

-

RBA says outlook for non-mining investment has improved

-

Low level of interest rates continuing to support the australian economy

-

Australian economy expected to grow around 3 pct in medium term

-

Labour market continues to strengthen

-

Household consumption is a source of uncertainty

-

Public infrastructure investment supporting economy

-

Unemployment rate expected to decline gradually

-

Rising A$ would result in slower economy, inflation

-

Says A$ remains within the range it has been over the past two years on trade-weighted basis

Based on provisional data, the Federal Statistical Office (Destatis) reports that price-adjusted new orders in manufacturing had increased in December 2017 a seasonally and working-day adjusted 3.8% on the previous month. For November 2017, revision of the preliminary outcome resulted in a decrease of 0.1% compared with October 2017 (primary -0.4%). Price-adjusted new orders without major orders in manufacturing had increased in December 2017 a seasonally and working-day adjusted +0.8% on the previous month.

In December 2017, domestic orders increased by 0.7% and foreign orders increased by 5.9% on the previous month. New orders from the euro area were up 11.2%, new orders from other countries increased 2.7% compared to November 2017.

European stocks finished sharply lower on Monday, tracking a global selloff in equities that picked up speed on Friday, after a better-than-expected U.S. jobs report stoked fears about rising inflation and higher interest rates.

U.S. stocks tumbled Monday, with the Dow recording its worst one-day point drop in history, in a selloff that at times took on the characteristics of a panic. The Dow was down more than 1,500 points at its session low, while the S&P 500 logged its first 5% pullback from its all-time high in over a year.

Japan's Nikkei index nosedived more than 6.5% on Tuesday, while Hong Kong's Hang Seng plummeted nearly 5%. Those sharp falls came after a brutal trading session in U.S. markets on Monday. The Dow closed down 1,175 points, or 4.6%. It was by far the index's biggest ever point decline for a single trading day.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers