- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-02-2018

Major US stock indices fell significantly on Friday, weighed down by weak earnings reports of blue chip companies, and also due to the fact that a reliable US employment report raised bond yields to multi-year highs to 2.85%. So, employment growth in the US accelerated in January, and wages increased, recording the largest annual profit for more than 8.5 years, confirming expectations that inflation will rise this year, as the labor market will reach full employment. The number of people employed in the non-agricultural sector jumped by 200,000 jobs last month after rising by 160,000 in December, the Ministry of Labor said on Friday. The unemployment rate was unchanged at the 17-year low of 4.1%. Average hourly earnings rose by nine cents, or 0.3%, in January to $ 26.74, after rising 0.4% in December. This increased the annual increase in the average hourly earnings to 2.9%, which is the biggest increase since June 2009 compared to 2.7% in December.

All components of the DOW index finished trading in the red (28 of 30). Outsider were shares of Exxon Mobil Corporation (XOM, -6.12%).

All sectors of the S & P index recorded a decline. The largest drop was shown by the main materials sector (-3.6%).

At closing:

Dow -2.54% 25,520.96 -665.75

Nasdaq -1.96% 7,240.95 -144.92

S & P -2.12% 2.762.13 -59.85

New orders for manufactured durable goods in December increased $7.0 billion or 2.9 percent to $249.4 billion, the U.S. Census Bureau announced today. This increase, up four of the last five months, followed a 1.7 percent November increase. Excluding transportation, new orders increased 0.6 percent. Excluding defense, new orders increased 2.2 percent. Transportation equipment, also up four of the last five months,led the increase, $6.0 billion or 7.4 percent to $87.2 billion.

Shipments of manufactured durable goods in December, up seven of the last eight months, increased $1.5 billion or 0.6 percent to $246.8 billion. This followed a 1.3 percent November increase. Fabricated metal products, also up seven of the last eight months, led the increase, $0.5 billion or 1.5 percent to $33.5 billion.

U.S. stock-index futures fell on Friday as strong U.S. labour market data bolstered expectations that inflation would push higher and pushed up bond yields further.

Global Stocks:

Nikkei 23,274.53 -211.58 -0.90%

Hang Seng 32,601.78 -40.31 -0.12%

Shanghai 3,462.94 +15.96 +0.46%

S&P/ASX 6,121.40 +31.30 +0.51%

FTSE 7,467.57 -22.82 -0.30%

CAC 5,392.36 -62.19 -1.14%

DAX 12,838.45 -165.45 -1.27%

Crude $65.81 (+0.02%)

Gold $1,342.10 (-0.43%)

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 245.46 | -2.48(-1.00%) | 1385 |

| ALCOA INC. | AA | 52 | -0.42(-0.80%) | 615 |

| ALTRIA GROUP INC. | MO | 69.71 | -0.22(-0.31%) | 1450 |

| Amazon.com Inc., NASDAQ | AMZN | 1,469.90 | 79.90(5.75%) | 240684 |

| American Express Co | AXP | 99.13 | -0.87(-0.87%) | 1024 |

| Apple Inc. | AAPL | 166.84 | -0.94(-0.56%) | 3185925 |

| AT&T Inc | T | 38.88 | -0.28(-0.72%) | 35001 |

| Barrick Gold Corporation, NYSE | ABX | 14.25 | -0.17(-1.18%) | 20325 |

| Boeing Co | BA | 355 | -1.94(-0.54%) | 23384 |

| Caterpillar Inc | CAT | 161.23 | -1.01(-0.62%) | 6002 |

| Chevron Corp | CVX | 122.51 | -3.06(-2.44%) | 93472 |

| Cisco Systems Inc | CSCO | 41.2 | -0.50(-1.20%) | 52985 |

| Citigroup Inc., NYSE | C | 79 | 0.12(0.15%) | 32408 |

| Deere & Company, NYSE | DE | 165.65 | -2.20(-1.31%) | 774 |

| Exxon Mobil Corp | XOM | 86.47 | -2.60(-2.92%) | 156839 |

| Facebook, Inc. | FB | 192.05 | -1.04(-0.54%) | 252649 |

| Ford Motor Co. | F | 10.87 | -0.05(-0.46%) | 70474 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 19.22 | -0.23(-1.18%) | 5063 |

| General Electric Co | GE | 15.91 | -0.11(-0.69%) | 448449 |

| General Motors Company, NYSE | GM | 42 | -0.43(-1.01%) | 4145 |

| Goldman Sachs | GS | 271.82 | -0.41(-0.15%) | 10288 |

| Google Inc. | GOOG | 1,130.63 | -37.07(-3.17%) | 28394 |

| Hewlett-Packard Co. | HPQ | 22.95 | -0.35(-1.50%) | 5638 |

| Home Depot Inc | HD | 198.9 | -1.00(-0.50%) | 4696 |

| HONEYWELL INTERNATIONAL INC. | HON | 158.9 | -0.75(-0.47%) | 599 |

| Intel Corp | INTC | 47.49 | -0.16(-0.34%) | 43223 |

| International Business Machines Co... | IBM | 161.87 | -0.53(-0.33%) | 9788 |

| Johnson & Johnson | JNJ | 139.05 | -0.97(-0.69%) | 7610 |

| JPMorgan Chase and Co | JPM | 117.23 | 0.36(0.31%) | 7955 |

| McDonald's Corp | MCD | 170.65 | -1.25(-0.73%) | 4092 |

| Merck & Co Inc | MRK | 59.75 | -0.11(-0.18%) | 15754 |

| Microsoft Corp | MSFT | 94.05 | -0.21(-0.22%) | 122233 |

| Nike | NKE | 67.13 | -0.52(-0.77%) | 1710 |

| Pfizer Inc | PFE | 36.6 | -0.23(-0.62%) | 17566 |

| Procter & Gamble Co | PG | 85.51 | -0.34(-0.40%) | 6972 |

| Starbucks Corporation, NASDAQ | SBUX | 55.75 | -0.25(-0.45%) | 10535 |

| Tesla Motors, Inc., NASDAQ | TSLA | 347 | -2.25(-0.64%) | 39279 |

| The Coca-Cola Co | KO | 47.19 | -0.26(-0.55%) | 5896 |

| Travelers Companies Inc | TRV | 149.18 | -0.82(-0.55%) | 1148 |

| Twitter, Inc., NYSE | TWTR | 26.87 | -0.27(-0.99%) | 129609 |

| United Technologies Corp | UTX | 136.32 | -2.00(-1.45%) | 1339 |

| UnitedHealth Group Inc | UNH | 233.23 | -1.99(-0.85%) | 1616 |

| Verizon Communications Inc | VZ | 54 | -0.30(-0.55%) | 2307 |

| Visa | V | 123 | -2.72(-2.16%) | 25377 |

| Wal-Mart Stores Inc | WMT | 105 | -0.52(-0.49%) | 6017 |

| Walt Disney Co | DIS | 109.65 | -0.84(-0.76%) | 6960 |

| Yandex N.V., NASDAQ | YNDX | 38.73 | -0.68(-1.73%) | 3200 |

Alphabet A (GOOGL) reiterated with a Buy at Needham; target $1,350

Alphabet A (GOOGL) target lowered to $1,350 from $1,375 B. Riley FBR; Buy

Alphabet A (GOOGL) downgraded to Hold from Buy at Stifel; target $1,150

HP (HPQ) downgraded to Neutral from Buy at Mizuho; target $23

Apple (AAPL) downgraded to Mkt Perform from Outperform at Bernstein

Apple (AAPL) downgraded to Sector Weight from Overweight at KeyBanc Capital Mkts

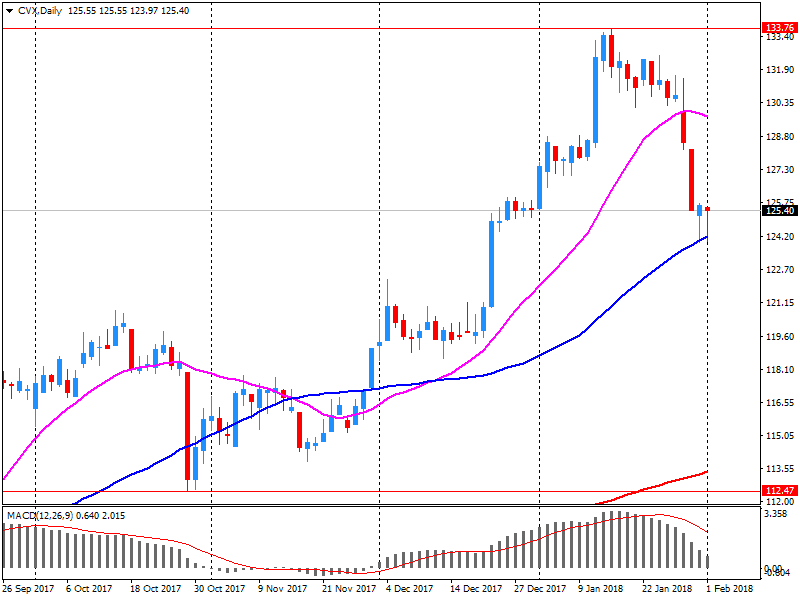

Chevron (CVX) reported Q4 FY 2017 earnings of $1.64 per share (versus $0.22 in Q4 FY 2016), may not be comparable to the analysts' consensus estimate of $1.24.

The company's quarterly revenues amounted to $37.616 bln (+19.4% y/y), missing analysts' consensus estimate of $38.425 bln.

The company's Board of Directors also approved a $0.04 per share increase in the quarterly dividend to $1.12 per share, payable in March 2018.

CVX fell to $122.12 (-2 75%) in pre-market trading.

In January, average hourly earnings for all employees on private nonfarm payrolls rose by 9 cents to $26.74, following an 11-cent gain in December. Over the year, average hourly earnings have risen by 75 cents, or 2.9 percent. Average hourly earnings of private-sector production and nonsupervisory employees increased by 3 cents to $22.34 in January.

Total nonfarm payroll employment increased by 200,000 in January, and the unemployment rate was unchanged at 4.1 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in construction, food services and drinking places, health care, and manufacturing.

In January, the unemployment rate was 4.1 percent for the fourth consecutive month. The number of unemployed persons, at 6.7 million, changed little over the month.

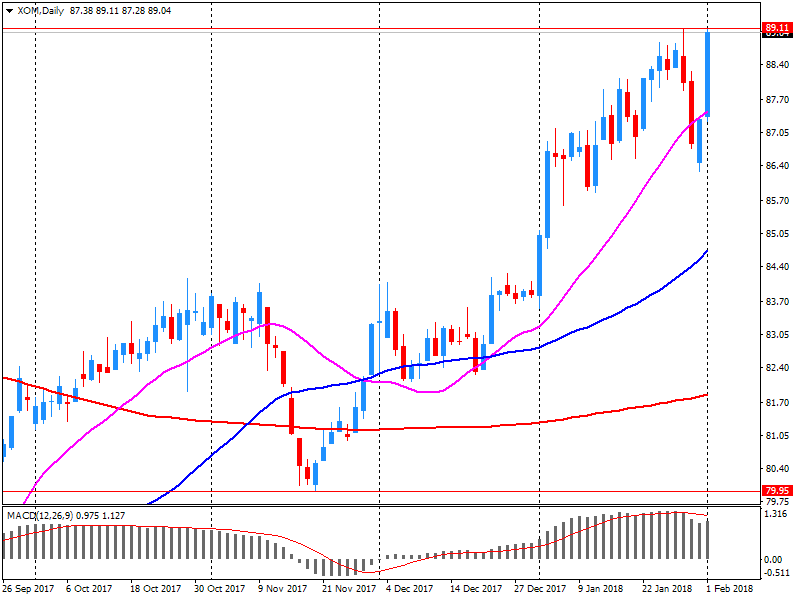

Exxon Mobil (XOM) reported Q4 FY 2017 earnings of $0.88 per share (versus $0.41 in Q4 FY 2016), missing analysts' consensus estimate of $1.03.

The company's quarterly revenues amounted to $66.515 bln (+9.0% y/y), missing analysts' consensus estimate of $74.408 bln.

XOM fell to $86.35 (-3.05%) in pre-market trading.

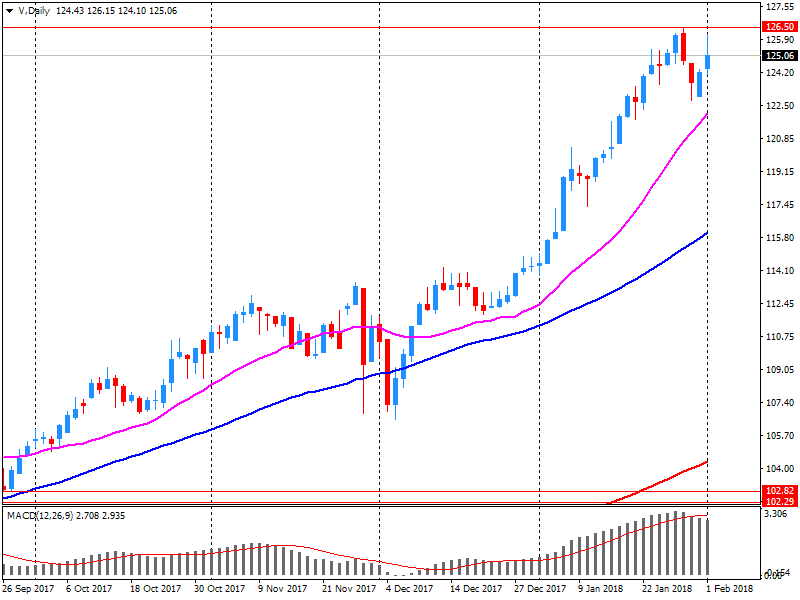

Visa (V) reported Q1 FY 2018 earnings of $1.08 per share (versus $0.86 in Q1 FY 2017), beating analysts' consensus estimate of $0.98.

The company's quarterly revenues amounted to $4.862 bln (+9.0% y/y), generally in-line with analysts' consensus estimate of $4.824 bln.

V fell to $123.60 (-1.69%) in pre-market trading.

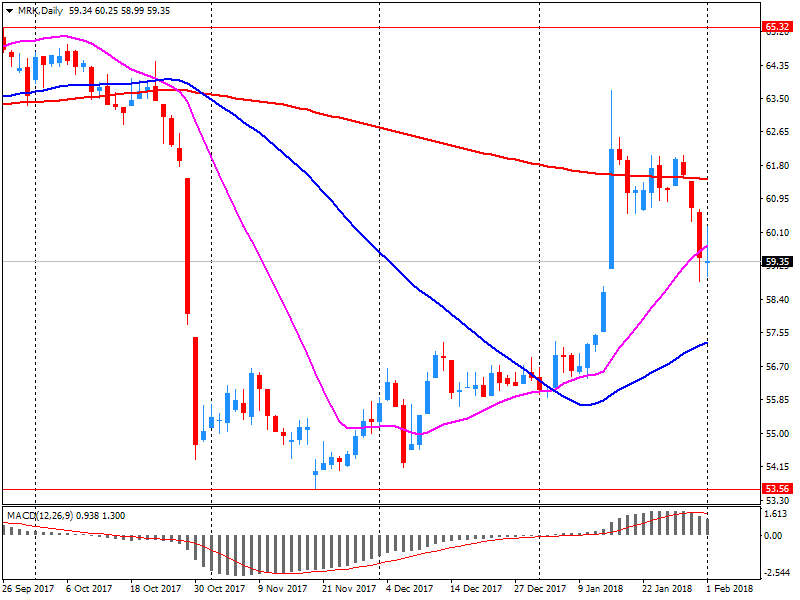

Merck (MRK) reported Q4 FY 2017 earnings of $0.98 per share (versus $0.89 in Q4 FY 2016), beating analysts' consensus estimate of $0.94.

The company's quarterly revenues amounted to $10.433 bln (+3.1% y/y), generally in-line with analysts' consensus estimate of $10.485 bln.

The company also issued guidance for FY 2018, projecting EPS of $4.08-4.23 (versus analysts' consensus estimate of $4.11) and revenues of $41.2-42.7 bln (versus analysts' consensus estimate of $41.1 bln).

MRK rose to $60.00 (+0.23%) in pre-market trading.

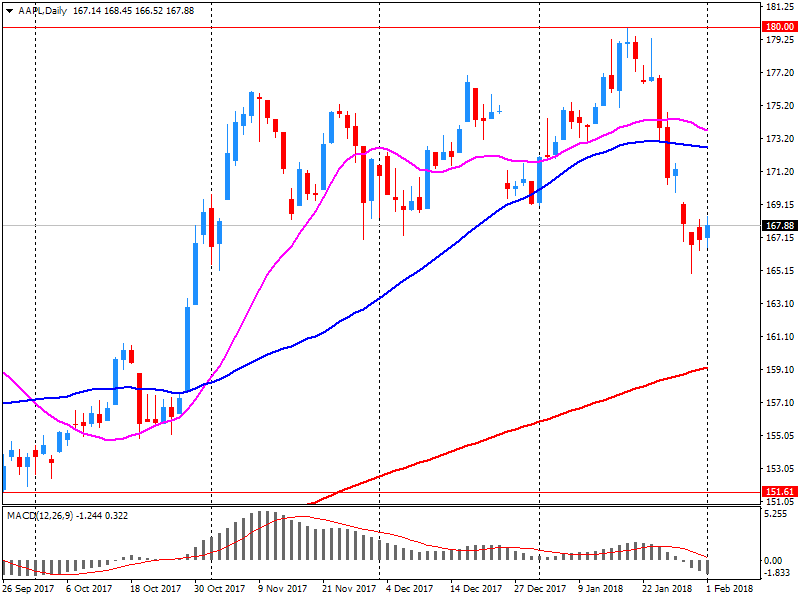

Apple (AAPL) reported Q1 FY 2018 earnings of $3.89 per share (versus $3.36 in Q1 FY 2017), beating analysts' consensus estimate of $3.85.

The company's quarterly revenues amounted to $88.293 bln (+12.7% y/y), generally in-line with analysts' consensus estimate of $87.617 bln.

AAPL rose to $169.25 (+0.88%) in pre-market trading.

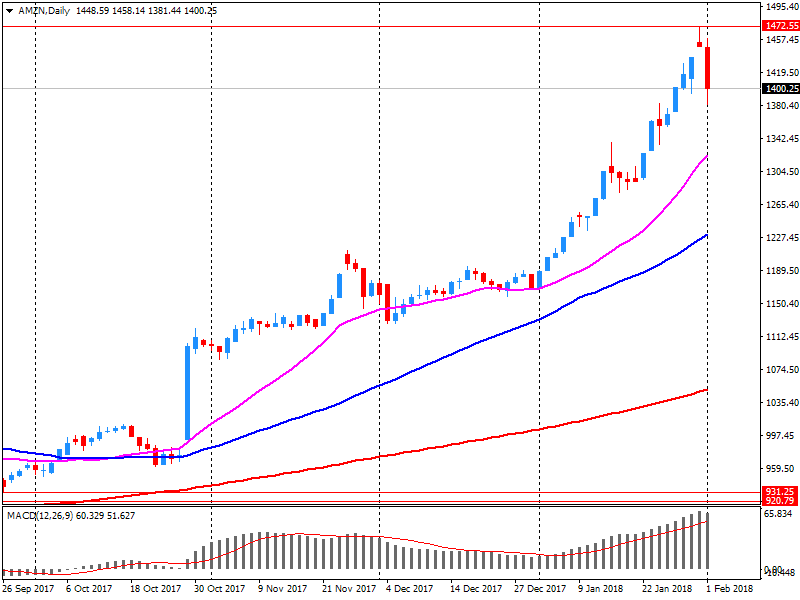

Amazon (AMZN) reported Q4 FY 2017 earnings of $2.19 per share (versus $1.54 in Q4 FY 2016), beating analysts' consensus estimate of $1.83.

The company's quarterly revenues amounted to $60.453 bln (+38.2% y/y), generally in-line with analysts' consensus estimate of $59.851 bln.

AMZN rose to $1472.40 (+5.93%) in pre-market trading.

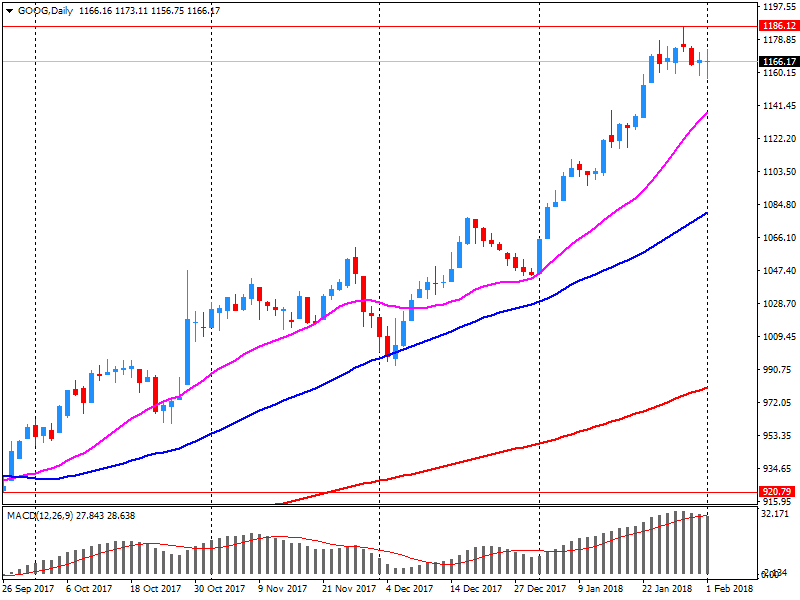

Alphabet (GOOG) reported Q4 FY 2017 earnings of $9.70 per share (versus $9.36 in Q4 FY 2016), missing analysts' consensus estimate of $10.07.

The company's quarterly revenues amounted to $32.323 bln (+24.0% y/y), beating analysts' consensus estimate of $31.879 bln.

GOOG fell to $1,131.00 (-3.14%) in pre-market trading.

UK construction companies reported a subdued start to 2018, with total industry activity barely rising. A return to contraction in residential building activity was accompanied by near-stagnant commercial and civil engineering activity.

New orders declined, linked by many companies to market uncertainty. On a more positive note, confidence towards future growth prospects improved, with many firms anticipating an increase in new project wins later in the year. Meanwhile, intense cost pressures continued across the UK construction sector.

The seasonally adjusted IHS Markit/CIPS UK Construction Purchasing Managers' Index posted 50.2 in January, down from 52.2 in December. The figure was just above the neutral 50.0 no-change mark, thereby signalling a fractional rate of growth that was the weakest for four months.

In December 2017, compared with November 2017, industrial producer prices rose by 0.2% in the euro area (EA19) and by 0.1% in the EU28, according to estimates from Eurostat, the statistical office of the European Union. In November 2017, prices increased by 0.6% in the euro area and by 0.7% in the EU28. In December 2017, compared with December 2016, industrial producer prices rose by 2.2% in the euro area and by 2.4% in the EU28. The average industrial producer prices for the year 2017, compared with 2016, increased by 3.1% in the euro area and by 3.4% in the EU28.

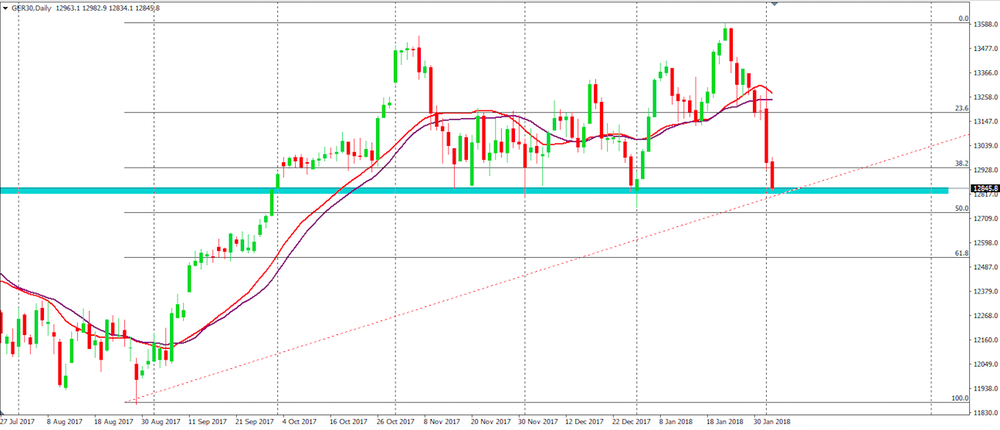

DAX has shown some indecision on the last few days.

On daily time frame chart, we can see that the price is stuck in a consolidation zone.

However, at this movement it is close to the bottom of the consolidation (which is a support level).

Therefore, if the price starts to reject more downside movements we can expect a further bullish movement soon.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2607 (2000)

$1.2583 (2410)

$1.2546 (1654)

Price at time of writing this review: $1.2505

Support levels (open interest**, contracts):

$1.2454 (959)

$1.2422 (1231)

$1.2384 (1030)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 9 is 141559 contracts (according to data from February, 1) with the maximum number of contracts with strike price $1,1850 (7036);

GBP/USD

Resistance levels (open interest**, contracts)

$1.4384 (954)

$1.4359 (262)

$1.4325 (748)

Price at time of writing this review: $1.4252

Support levels (open interest**, contracts):

$1.4203 (109)

$1.4147 (216)

$1.4112 (455)

Comments:

- Overall open interest on the CALL options with the expiration date February, 9 is 47199 contracts, with the maximum number of contracts with strike price $1,3600 (3462);

- Overall open interest on the PUT options with the expiration date February, 9 is 43865 contracts, with the maximum number of contracts with strike price $1,3400 (3038);

- The ratio of PUT/CALL was 0.93 versus 0.95 from the previous trading day according to data from February, 1

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

Final demand (excl. Exports):

Rose 0.6% in the december quarter 2017.

Mainly due to rises in the prices received for petroleum refining and petroleum fuel manufacturing (+11.9%), heavy and civil engineering construction (+0.7%) and building construction (+0.4%).

Partly offset by falls in the prices received for sugar and confectionery manufacturing (-3.9%), tobacco product manufacturing (-3.8%) and sheep, beef cattle and grain farming; and dairy cattle farming (-3.6%).

Rose 1.7% through the year to the december quarter 2017.

Intermediate demand:

Rose 1.2% in the december quarter 2017.

Mainly due to rises in the prices received for electricity, gas and water supply (+2.9%), petroleum refining and petroleum fuel manufacturing (+11.3%) and oil and gas extraction (+14.5%).

Partly offset by falls in the prices received for textile, leather, clothing and footwear manufacturing (-1.5%), motor vehicle and part manufacturing (-1.9%) and sugar and confectionery manufacturing (-7.6%).

Rose 3.1% through the year to the december quarter 2017.

European stock gauges finished with sizable losses Thursday as February kicked off, falling for a fourth session in a row as global bond yields extended their recent climb. The Stoxx Europe 600 index SXXP, -0.50% dropped 0.5% to end at 393.52, turning negative after a morning gain. It closed at a four-week low, cutting its 2018 gain to 1.1%.

U.S. stock indexes ended mostly lower on Thursday, switching between gains and losses as fears of a pick up in inflation and rising bond yields fostered emerging volatility on Wall Street.

Stock indexes in Japan and South Korea suffered earnings-related hits Friday, with Samsung Electronics falling 3.5% after rival Apple's latest quarterly financial results. Apple AAPL, +0.21% reported a slight drop in iPhone sales in the three months through December and gave a downbeat revenue forecast for the current quarter.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers